%20copy%202.png)

How Every State Can Create a Digital Equity and Opportunity Dividend with Available BEAD Funding

September 18, 2024

Last week, Vernonburg Group submitted comments in response to the National Telecommunications and Information Administration’s Policy Notice on how best to provide Broadband Equity, Access, and Deployment (BEAD) program funding to Internet service providers (ISPs) deploying alternative broadband technologies – i.e., unlicensed fixed wireless or low earth orbit satellite technologies – in places where end-to-end fiber and other reliable broadband services prove infeasible.

In our comments, we shared estimates from Vernonburg Group’s free Broadband Funding Optimization Tool that demonstrates how there is sufficient funding available for states and territories so they can achieve Internet for All by establishing a reasonable upper limit on what they are willing to spend per-location. This does mean, however, that states and territories will need to consider not only deployment of end-to-end fiber networks and other reliable broadband services, but also other, less costly qualifying alternative broadband technologies. If they do so, states and territories can preserve sufficient funding to connect all remaining unserved and underserved locations as well as connect CAIs and fund digital equity/digital opportunity programs.

The Broadband Funding Optimization Tool demonstrates that to achieve these goals state and territorial broadband offices need to set their Extremely High Cost Per Location Thresholds at levels that place a reasonable upper per-location limit on what they are willing to spend on end-to-end fiber builds. Each state’s Extremely High Cost Per Location Threshold will be different based on a variety of factors, but all states and territories can set their Extremely High Cost Per Location Threshold at a level that enables them to achieve Internet for All using a mix of fiber, fixed wireless, and satellite technologies. For example, the default view of the Tool shows that, if states and territories collectively chose to set aside 10 percent of available funds for connecting community anchor institutions (CAIs) and funding digital equity programs, they could still extend high-speed broadband to all unserved and underserved locations.

As of August 2024, according to the Federal Communications Commission’s (FCC’s) Broadband Data Collection, there are approximately 7.0 million locations that lack access to broadband services that meet the minimum speed of 100/20 Mbps required under the Infrastructure Investment and Jobs Act to be considered served. Of those, 4.5 million are unserved and 2.5 million are underserved. The Broadband Funding Optimization Tool shows that the cost of extending end-to-end fiber to every unserved and underserved location would be approximately $119 billion, far exceeding available public and private funding, meaning a “one-technology fits all” approach does not work. Instead, the Broadband Funding Optimization Tool’s default view shows that, to achieve Internet for All approximately, 62.9 percent or 4.4 million locations could be served with end-to-end fiber connections, 32.5 percent or 2.3 million locations could be served with fixed wireless, and the remaining 4.6 percent or 324,025 locations would be served with satellite.

As we note in the accompanying Inputs and Assumptions document, the Broadband Funding Optimization Tool optimistically assumes that prospective ISP subgrantees will be willing to bid up to $20,000 for a location served by end-to-end fiber and up to $10,000 for a location service by fixed wireless. With a required 25 percent private sector match minimum, that means the prospective ISP subgrantee must be willing to contribute up to $5,000 toward the cost of an end-to-end fiber connection and up to $2,500 toward the cost of a fixed wireless connection. It is very possible that ISPs and their investors will be unwilling to spend this much; reasons for this include increasingly constrained capital markets, opportunities to invest funds in less costly markets free from the BEAD program’s regulatory overhead, and the high costs of ongoing operations in rural and low-density areas which the BEAD program will not support.

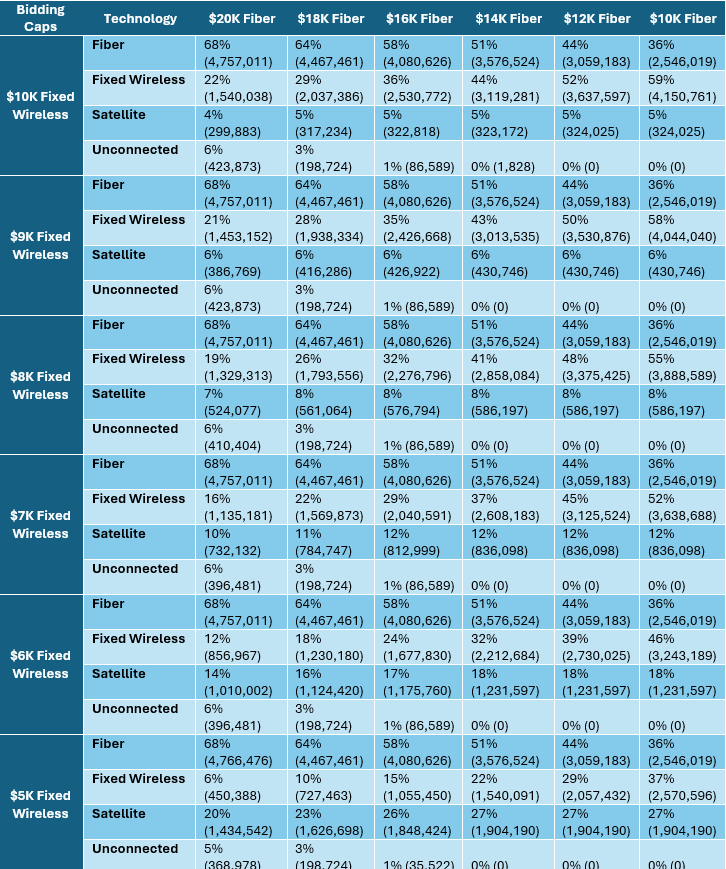

The Broadband Funding Optimization Tool allows users to see how the mix of technologies used to extend high-speed broadband to every unserved and underserved location will change as prospective ISP subgrantees change the upper limit they are willing to bid on a per location basis for end-to-end fiber and fixed wireless deployments. The table below shows the outcome of different bidding scenarios.

The table shows how the mix of fiber, fixed wireless, and satellite technologies changes as maximum bids decline. If, for example, prospective ISP subgrantees were only willing to bid up to $10,000 per location (i.e., not greater than a $2,500 match) for end-to-end fiber and up to $5,000 (i.e., not greater than a $1,250 match) per location for fixed wireless, then approximately 36 percent or 2.55 million locations could be served with end-to-end fiber connections, 37 percent or 2.57 million locations could be served with fixed wireless, and the remaining 27 percent or 1.9 million locations would be served with satellite. The percentage of locations served by fiber, fixed wireless, and satellite technology becomes roughly equal under this scenario, a radically different outcome than if ISPs were willing to invest much more.

At this point, nobody can predict exactly how the BEAD program will play out or what bidders will bid. Each state and territory will need to go through its BEAD subgrantee selection process before this picture becomes clearer. What we can say with certainty is that all qualified technologies will be necessary to close the digital divide and achieve the Internet for All envisioned by NTIA for the BEAD program. We can also say with certainty that if the mix of technologies is optimized, states and territories have a real opportunity to connect more CAIs and advance their digital equity/digital opportunity goals with a substantial injection of additional funding – the Digital Equity and Opportunity Dividend.